Does Royal Mail (LON:RMG) Have A Healthy Balance Sheet? – Simply Wall St News

[ad_1]

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Royal Mail plc (LON:RMG) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Royal Mail

What Is Royal Mail’s Net Debt?

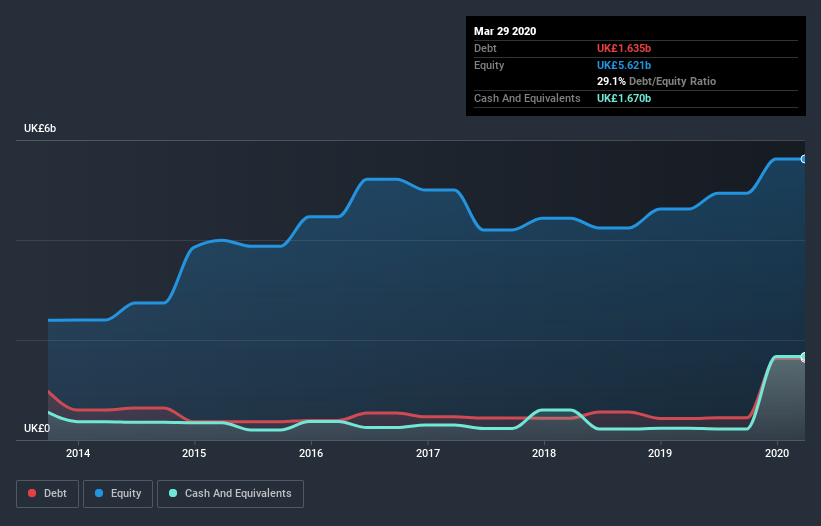

The image below, which you can click on for greater detail, shows that at March 2020 Royal Mail had debt of UK£1.64b, up from UK£431.0m in one year. But on the other hand it also has UK£1.67b in cash, leading to a UK£35.0m net cash position.

How Strong Is Royal Mail’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Royal Mail had liabilities of UK£3.10b due within 12 months and liabilities of UK£2.30b due beyond that. On the other hand, it had cash of UK£1.67b and UK£1.20b worth of receivables due within a year. So it has liabilities totalling UK£2.5b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company’s market capitalization of UK£1.72b, we think shareholders really should watch Royal Mail’s debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution. Royal Mail boasts net cash, so it’s fair to say it does not have a heavy debt load, even if it does have very significant liabilities, in total.

The modesty of its debt load may become crucial for Royal Mail if management cannot prevent a repeat of the 32% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Royal Mail’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Royal Mail may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Royal Mail actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing up

Although Royal Mail’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of UK£35.0m. The cherry on top was that in converted 118% of that EBIT to free cash flow, bringing in UK£608m. Despite the cash, we do find Royal Mail’s EBIT growth rate concerning, so we’re not particularly comfortable with the stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We’ve spotted 2 warning signs for Royal Mail you should be aware of.

If, after all that, you’re more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Promoted

If you decide to trade Royal Mail, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

These great dividend stocks are beating your savings account

Not only have these stocks been reliable dividend payers for the last 10 years but with the yield over 3% they are also easily beating your savings account (let alone the possible capital gains). Click here to see them for FREE on Simply Wall St.

[ad_2]

Source link