Stock market stalwarts face reinvention test

[ad_1]

Very old companies tend to fall into one of two categories. Some provide solutions to everyday problems or needs. Coats (COA), which has been manufacturing industrial thread since 1755, is a good example of this. Whatever the century, people have always required clothes, and clothes have always required thread. The second group consists of skillful shapeshifters, who are good at adapting and expanding with the times. Enter Intertek (ITRK), which started life 130 years ago certifying grain cargoes and now quality checks everything from cosmetics to aeroplanes.

A small number of businesses fall between two stools, however. After decades of success, they have watched demand for their services wane, but cumbersome legacy structures have made reinvention difficult. Royal Mail (RMG) and De La Rue (DLAR) occupy this awkward middle ground and both are now in the throes of turnaround plans. But whether they can keep up with the modern world hangs in the balance.

Royal Mail’s roadblock

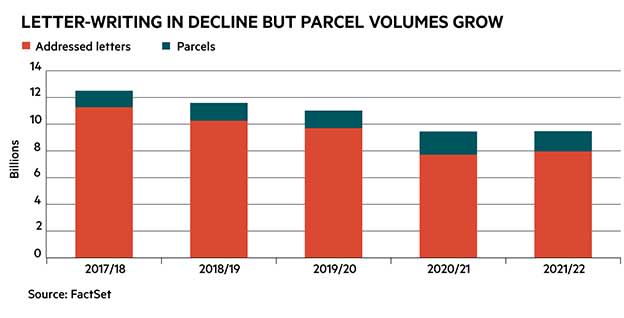

Royal Mail is a British icon. Having started life in 1516 when Henry VIII was on the throne, it has witnessed the invention of stamps in 1840, postcodes in 1959 and drone delivery routes in 2022. It’s no surprise that a courier with so much history comes with some baggage. Since being privatised in 2013, Royal Mail has been a shaky source of returns for investors, squeezed by ultra-efficient rivals and a fall off in letter-writing.

Its transformation plan, which was announced in 2019 and aims to boost efficiency, is starting to bear fruit. The year to 28 March 2021 was an excellent period for the group, with parcel volumes soaring, pre-tax profits quadrupling, and the shares increasing threefold.

Revenue in the year to 27 March 2022 also proved strong, and total operating costs decreased by 2.5 per cent. Management has identified future savings of £350mn, including from job cuts, route improvements and automation.

The group’s dazzling renaissance might be too good to be true, however. Volumes of addressed letters are falling fast, down 18 per cent compared with pre-pandemic levels, and parcel volumes are also starting to wobble.

“Having come out of Covid, it’s quite likely that parcel volumes will decline in the current financial year,” said Peel Hunt analyst Alexander Paterson. “This reduction is because consumers are being squeezed, so real disposable income is lower, and also because international parcels have been hit very hard by a number of factors, including Brexit.”

A fall in deliveries spells trouble – particularly given Royal Mail’s high operational gearing. If posties have one fewer parcel or letter to deliver everyday, fixed costs will stay largely the same. However, such a fall would have a substantial effect on revenue, and thus on profits. It is a different story for modern couriers such as Evri (formerly Hermes) and Yodel, who typically pay drivers for every package they deliver.

“High operational gearing means lower revenues cannot be fully mitigated by cost avoidance and risks further downside to estimates,” Paterson said.

Plus, there’s only so much fat the courier is allowed to trim. Unlike its younger rivals, Royal Mail is bound by a ‘universal service obligation’, as set out in the Postal Services Act 2011. This means it must deliver to every address in the UK, six days a week, at a uniform price. So while some companies focus on densely populated urban areas, Royal Mail must cover the breadth of the country, regardless of cost.

The power wielded by staff also allows little wriggle room. People costs at Royal Mail amount to a hefty £5.6bn, but restructuring schemes are hard to implement due to the group’s highly unionised workforce. The group is currently locked in talks with trade unions over redundancies and pay deals, after it announced plans to sack over 1,000 managers. A strike has been threatened.

A loyal, if expensive, workforce has its benefits, however. As discussed in our recent ‘Lessons from the world’s oldest companies’ piece, there appears to be a direct correlation between employee retention and stock returns: Morgan Stanley’s Counterpoint Partners found that the top quintile of companies for employee retention enjoyed 25 per cent higher share gains than the bottom quintile.

Royal Mail’s balance sheet is also surprisingly strong, and its management team is well placed to handle the challenges. Executive chairman Keith Williams was chief executive of British Airways between 2011 and 2016. Pressure from unions and contracts drawn up in a bygone era will come as nothing new.

One course of action would be to alter the universal service obligation, and cut back delivery days. This would require agreement from communications regulator Ofcom and posties themselves, however, which may not be forthcoming. Indeed, trade union Unite has already shown signs of resistance, claiming that Royal Mail’s “real plan” is to eventually move to the three-day service model to appease “shareholder greed”.

Cash still king at De La Rue

De La Rue is younger than Royal Mail, at just over 200 years old. However, as a designer and printer of bank notes which sold its first products before Queen Victoria took the throne, it has similarly been integral to day-to-day life in the UK.

Much like Royal Mail, De La Rue has been stung by digitisation: paper banknotes are now almost as unfashionable as paper letters. As a result, the company has launched two turnaround plans in the past seven years. So far, however, neither has managed to drag the group’s shares out of a sustained nose dive that began in 2018.

Seven years ago, management decided to wean itself off currency and to diversify the group’s portfolio. Things went awry in 2018, however, when De La Rue lost its passport contract with the UK government to a Franco-Dutch firm. The following year saw a big hit from the Venezuelan central bank running out on an £18mn bill, a public spat with one of its largest shareholders, two profit warnings, an overhaul of senior management, a Serious Fraud Office investigation (closed without any prosecutions) and a warning about its ability to continue as a going concern.

Things have improved since then. The group is now phasing out its passport arm and has rediscovered its passion for banknotes – albeit polymer ones. In May of this year, however, management was forced to warn on profits once again, blaming supply chain issues, Covid-related absences and inflation. Ironically for a group that has struggled to adapt to the 21st century, it has even been hit by semiconductor shortages. (What remains of its passport arm uses embedded smart chips, which have experienced delivery delays.)

While Royal Mail requires a large workforce, De La Rue needs a lot of physical kit, including a vast factory in Essex which prints several million banknotes each day. The incremental cost of printing each bank note is fairly low and the physical assets are hard to shift, so it makes sense to maximise capacity as much as possible.

Customers are not playing ball, however. After a surge in demand for banknotes during the pandemic, governments have reined in their orders. In a bid to stoke demand, rivals such as Crane Currency – a subsidiary of US listed Crane Co. – and France’s Oberthur could switch to aggressive pricing strategies to increase market share. In a time of high inflation, this threatens to be a painful process.

Rising costs aren’t the only thing to keep an eye on; pensions often prove expensive for stock market veterans, too. AstraZeneca (AZ), founded in 1913, and Phoenix (PHNX), founded in 1857, have two of the biggest pension deficits in the FTSE 350, according to Investors’ Chronicle analysis. De La Rue is no exception, with a deficit of almost £120mn that requires annual payments of £15m until March 2029. This is lower than previously feared, after a new actuarial valuation revealed a reduced deficit, saving the company £57mn in cash payments.

The real risk for old companies toiling with transformation, however, seems to be too much innovation. In the depths of its full-year results, De La Rue mentions that “digital currencies remain an area of ongoing interest for many central banks”. While digital currencies are typically associated with volatile crypto-tokens, De La Rue is here referring to state-backed electronic money that could be spent on normal purchases – a version of online cash that is less trackable than debit or credit cards.

There’s a lot of government interest in this despite broad misgivings: a joint taskforce between the Bank of England and HM Treasury was set up last April to consider a digital currency for the UK, and around 90 other central banks are currently looking at the issue. Enthusiasm has been fuelled by concerns that tech giants will invent their own currencies and destabilise existing financial systems.

De La Rue says it has been working closely with technology providers and central banks to develop its position in this area. If there is a shift towards digital money, however, a company rooted in physical manufacturing may not be best placed for success. More prosaically, it’s also worth noting that plastic banknotes last significantly longer than paper ones, and therefore don’t need replacing as often. Management is confident that demand will remain strong for a while yet, but there is a lingering worry that De La Rue’s polymer creation is a bit too clever for its own good.

It’s not all doom and gloom. It’s clear, for example, that the group’s turnaround plan – like Royal Mail’s – is making a difference. Revenue from the currency division dipped in 2022, but adjusted operating profit still rose by a fifth. If demand does bounce back to normal levels, profit growth could quickly accelerate.

It’s also important to remember that while current conditions are challenging, this is not the first storm old companies have faced. Both are still left with strong assets and for Royal Mail this is backed up by its legal duties to deliver the mail (although it is working to get this dropped from six days a week, according to the Unite union).

Overall, corporate longevity is in decline, with one consultancy predicting that average tenure of S&P 500 companies will shrink to 15-20 years this decade, down from 30-35 years in the 1970s. The business of survival, therefore, seems to be getting more complicated. Those with more than two hundred years of trading under their belt might prove to have more stamina than most.

[ad_2]

Source link