The past year for Royal Mail (LON:RMG) investors has not been profitable

[ad_1]

The simplest way to benefit from a rising market is to buy an index fund. But if you buy individual stocks, you can do both better or worse than that. Investors in Royal Mail plc (LON:RMG) have tasted that bitter downside in the last year, as the share price dropped 46%. That contrasts poorly with the market decline of 5.8%. On the bright side, the stock is actually up 29% in the last three years. Shareholders have had an even rougher run lately, with the share price down 14% in the last 90 days.

It’s worthwhile assessing if the company’s economics have been moving in lockstep with these underwhelming shareholder returns, or if there is some disparity between the two. So let’s do just that.

However if you’d rather see where the opportunities and risks are within RMG’s industry, you can check out our analysis on the XX Logistics industry.

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

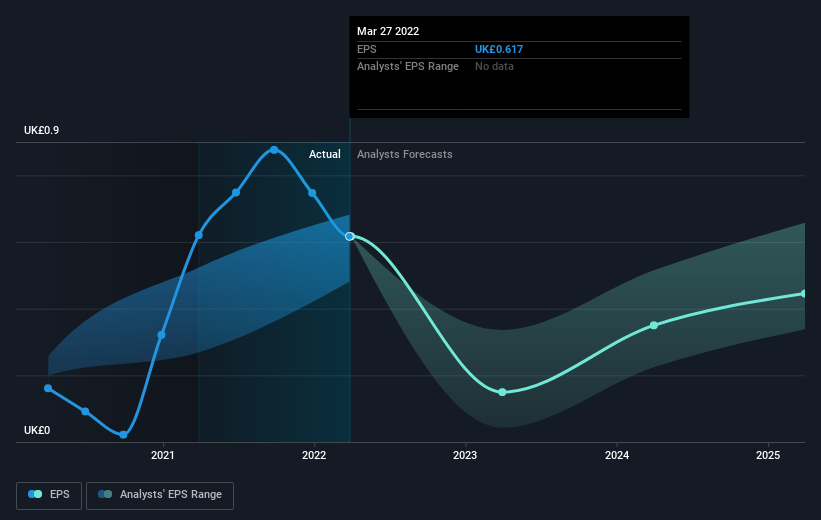

Unfortunately Royal Mail reported an EPS drop of 0.06% for the last year. This reduction in EPS is not as bad as the 46% share price fall. So it seems the market was too confident about the business, a year ago. The less favorable sentiment is reflected in its current P/E ratio of 4.13.

You can see below how EPS has changed over time (discover the exact values by clicking on the image).

We’re pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. It’s always worth keeping an eye on CEO pay, but a more important question is whether the company will grow earnings throughout the years. This free interactive report on Royal Mail’s earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. It’s fair to say that the TSR gives a more complete picture for stocks that pay a dividend. In the case of Royal Mail, it has a TSR of -40% for the last 1 year. That exceeds its share price return that we previously mentioned. This is largely a result of its dividend payments!

A Different Perspective

We regret to report that Royal Mail shareholders are down 40% for the year (even including dividends). Unfortunately, that’s worse than the broader market decline of 5.8%. Having said that, it’s inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. Regrettably, last year’s performance caps off a bad run, with the shareholders facing a total loss of 1.1% per year over five years. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Like risks, for instance. Every company has them, and we’ve spotted 2 warning signs for Royal Mail (of which 1 is a bit unpleasant!) you should know about.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Discounted cash flow calculation for every stock

Simply Wall St does a detailed discounted cash flow calculation every 6 hours for every stock on the market, so if you want to find the intrinsic value of any company just search here. It’s FREE.

[ad_2]

Source link